If you’re looking for a modern, online-first banking solution with strong savings rates and flexible credit options, Synchrony Bank is one of the most widely used names in the U.S. financial space. But is it actually worth using in 2026?

This in-depth guide breaks down everything you need to know — from savings accounts and credit cards to pros, cons, and who it’s best for.

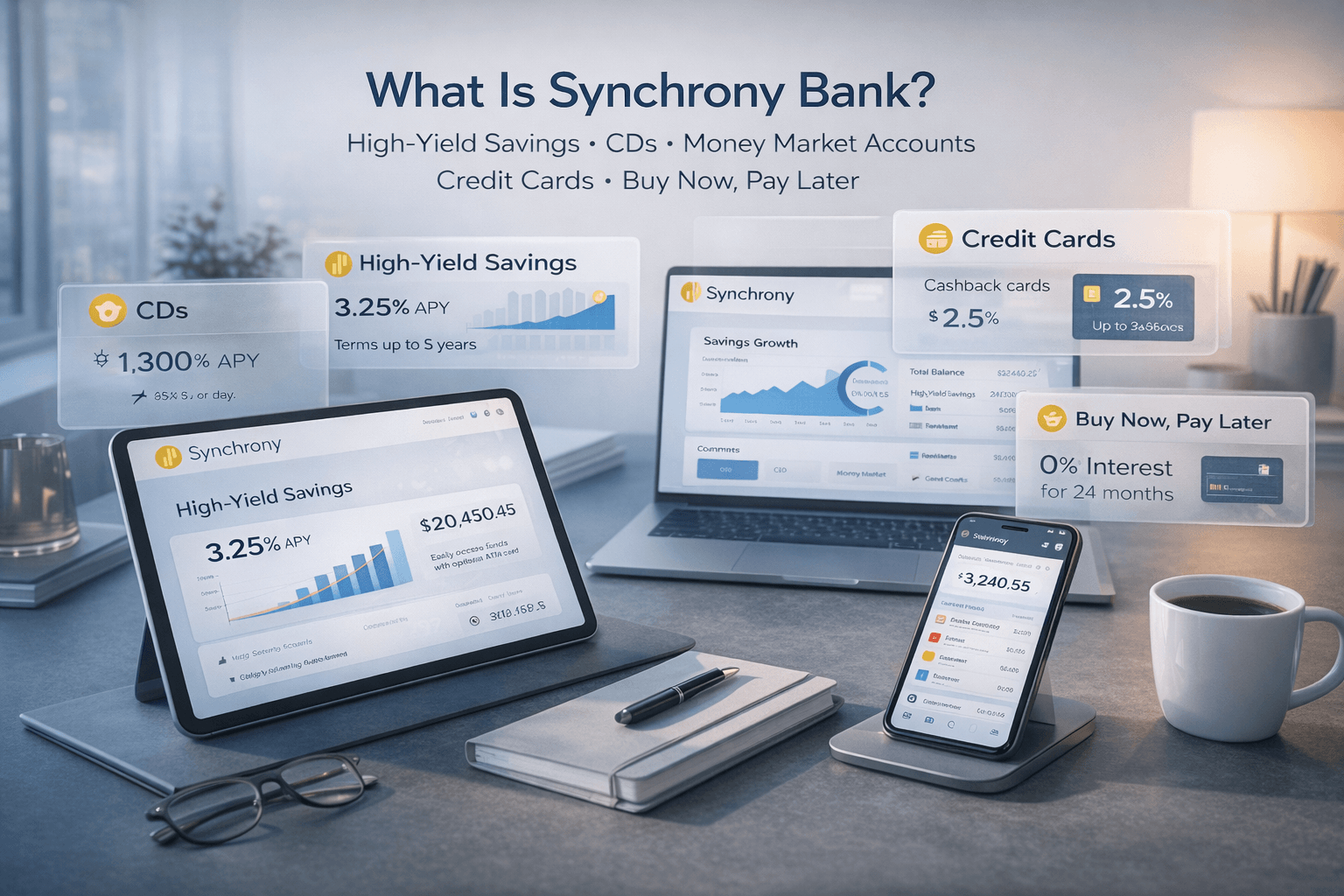

What Is Synchrony Bank?

Synchrony Bank is a U.S.-based online bank owned by Synchrony Financial. It focuses primarily on:

- High-yield savings products

- Certificates of deposit (CDs)

- Money market accounts

- Retail and co-branded credit cards

- Buy Now, Pay Later (BNPL) financing

Unlike traditional banks, Synchrony operates primarily online, with very limited physical locations.

Key Features at a Glance

- FDIC-insured up to $250,000

- No monthly fees on most accounts

- No minimum balance requirements

- Competitive interest rates (often above national average)

- Strong partnerships with major retailers

Synchrony Bank Products (2026)

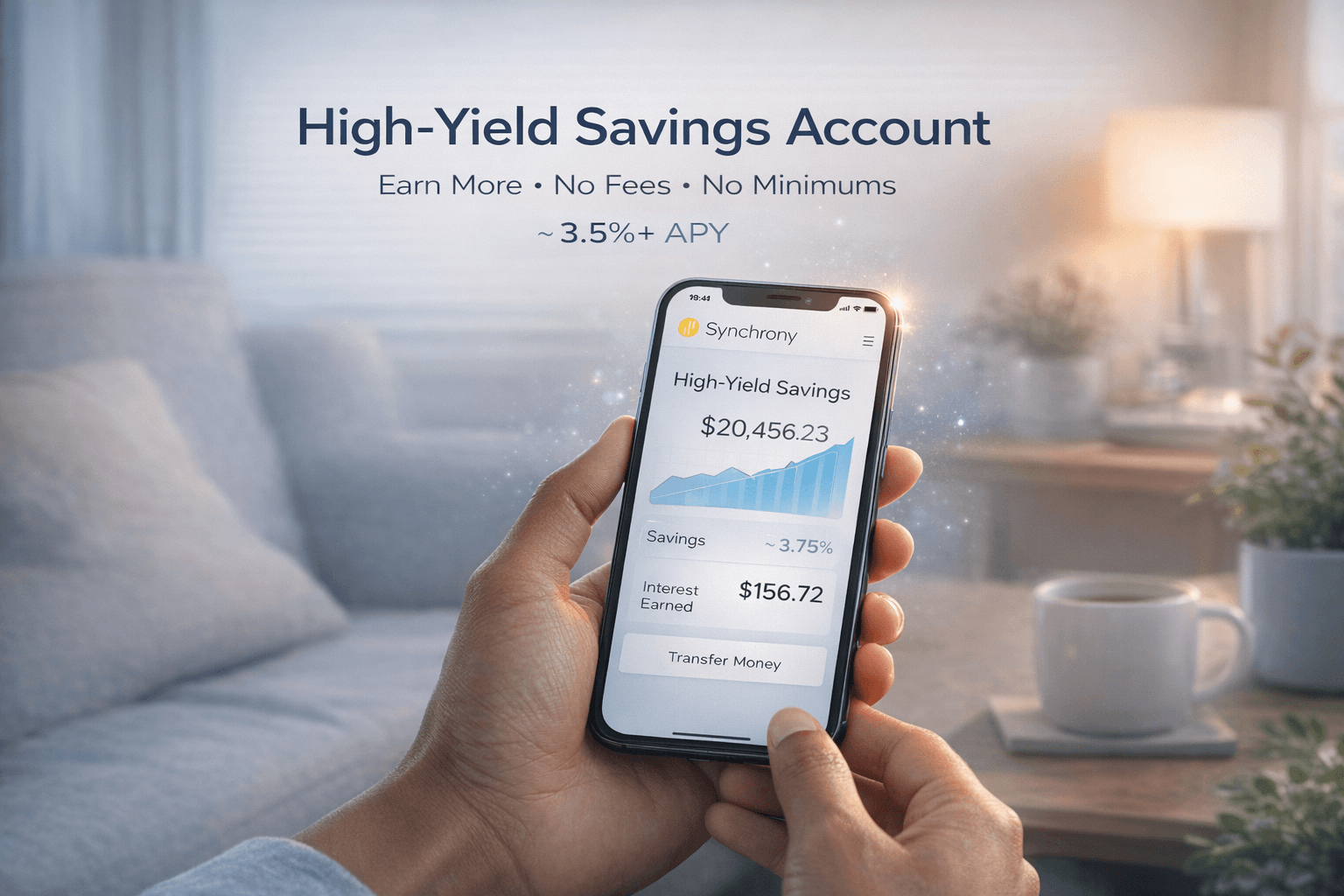

1. High-Yield Savings Account

One of Synchrony’s biggest strengths.

What you get:

- Competitive APY (around 3.5%+ range depending on market conditions)

- No minimum deposit

- No monthly fees

- Optional ATM card + fee reimbursements

Why it stands out:

Synchrony consistently ranks among top online savings accounts due to its high rates and zero fees.

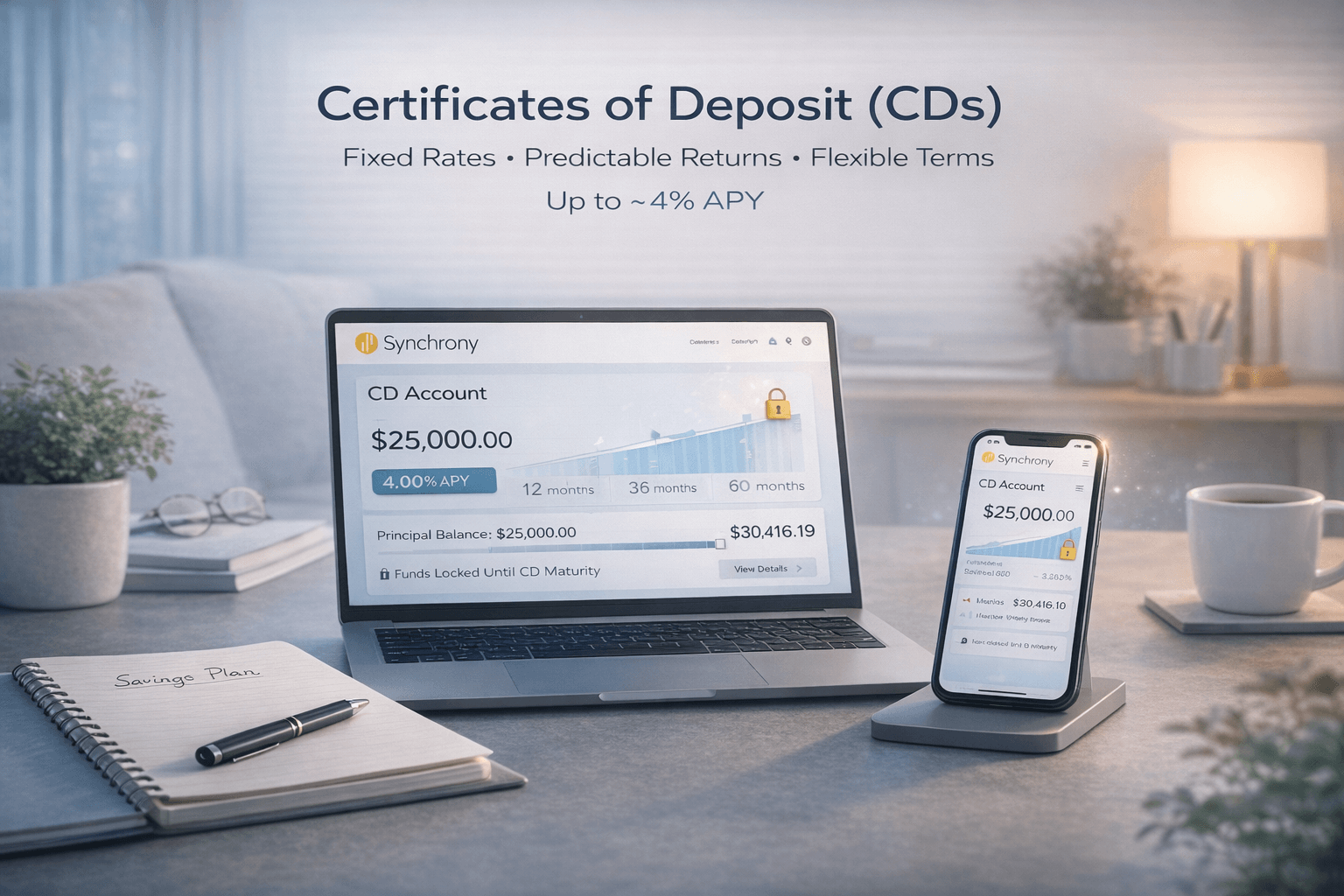

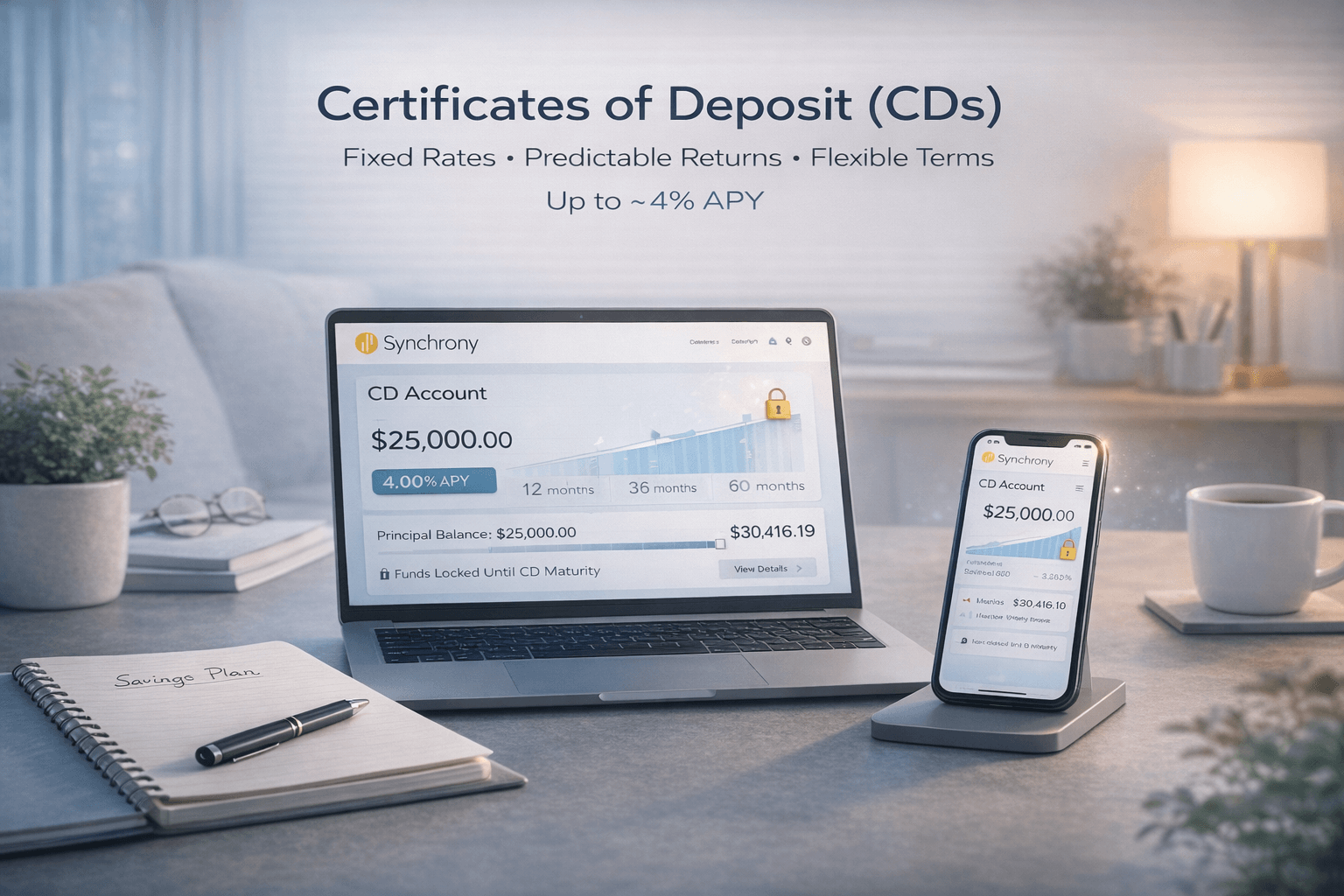

2. Certificates of Deposit (CDs)

Ideal for locking in higher returns.

Key features:

- Terms from 3 months to 5 years

- Rates up to ~4%+ APY depending on term

- No minimum balance

- IRA CD options available

Best for:

Long-term savers who don’t need immediate access to funds.

3. Money Market Account

A hybrid between savings and checking.

Includes:

- Competitive APY (~2% range)

- Check-writing ability

- ATM access

Trade-off:

Lower rates than savings accounts, but more flexibility.

4. Credit Cards & Financing

This is where Synchrony really stands out.

Synchrony powers store cards and financing for major brands like:

It also offers:

- Cashback cards

- Promotional financing (0% interest periods)

- Buy Now, Pay Later (Synchrony Pay)

Fees & Rates (2026)

| Feature | Synchrony Bank |

| Monthly fees | $0 |

| Minimum balance | $0 |

| Savings APY | ~3.5%+ |

| CD APY | Up to ~4%+ |

| ATM fee refund | Up to $5/month |

User Experience & Reviews

What people like:

- “Good rates… app seems really good”

- Strong long-term savings performance

Common complaints:

- Customer service issues

- Credit limit changes

- Difficulty linking external accounts

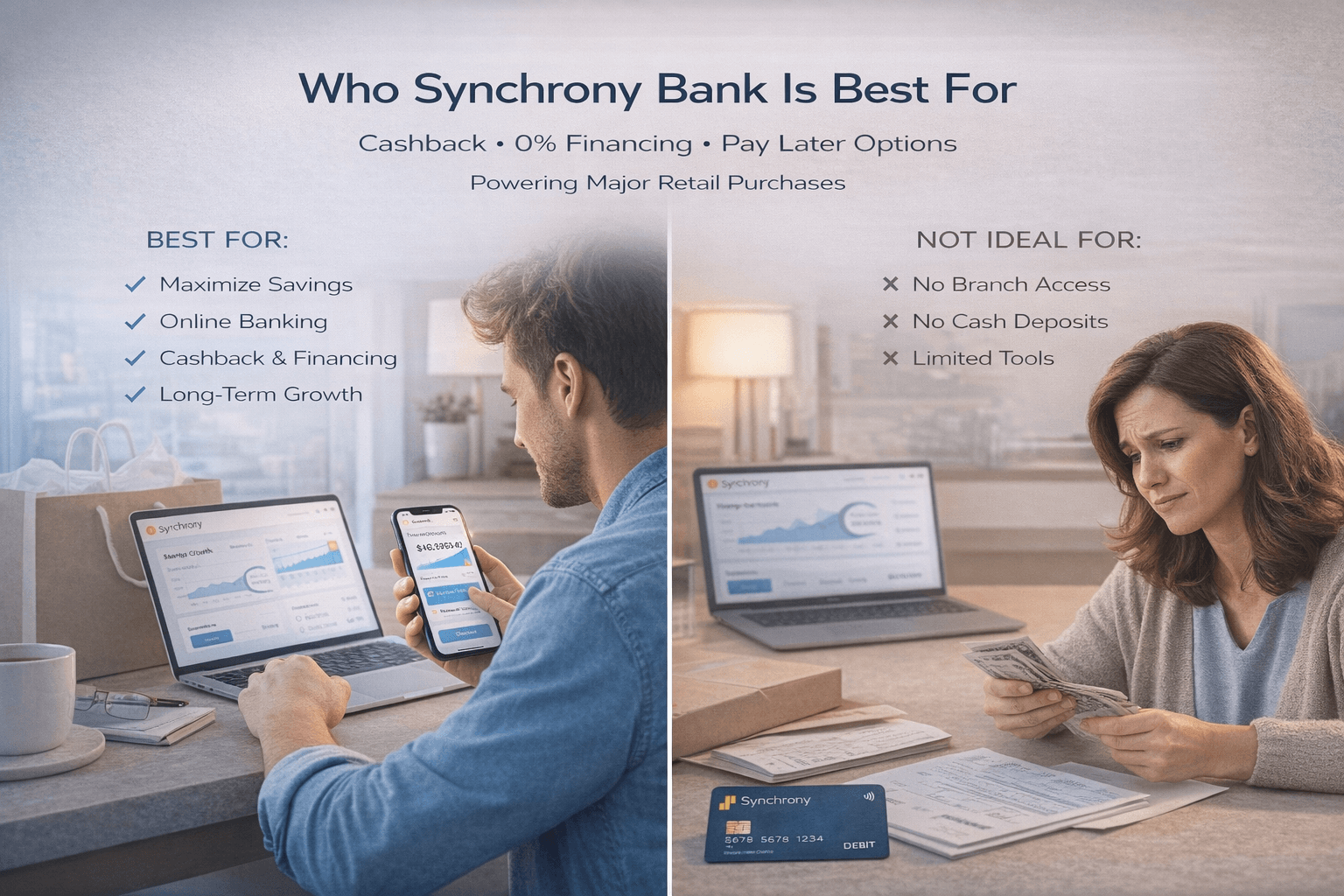

Who Synchrony Bank Is Best For

Best for:

- People focused on maximizing savings interest

- Users comfortable with online-only banking

- Shoppers who want store financing or cashback cards

- Long-term savers using CDs or IRAs

Not ideal for:

- People who want a full-service bank (checking + branches)

- Users needing cash deposits

- Those wanting advanced budgeting tools

Synchrony vs Traditional Banks

| Feature | Synchrony Bank | Traditional Bank |

| Interest rates | High | Low |

| Fees | Low / none | Often higher |

| Branch access | No | Yes |

| Checking account | No | Yes |

| Convenience | Online-focused | In-person + online |

Is Synchrony Bank Safe?

Yes. Synchrony Bank is:

- FDIC insured

- Backed by a Fortune 500 financial company

- Operating for over 80+ years

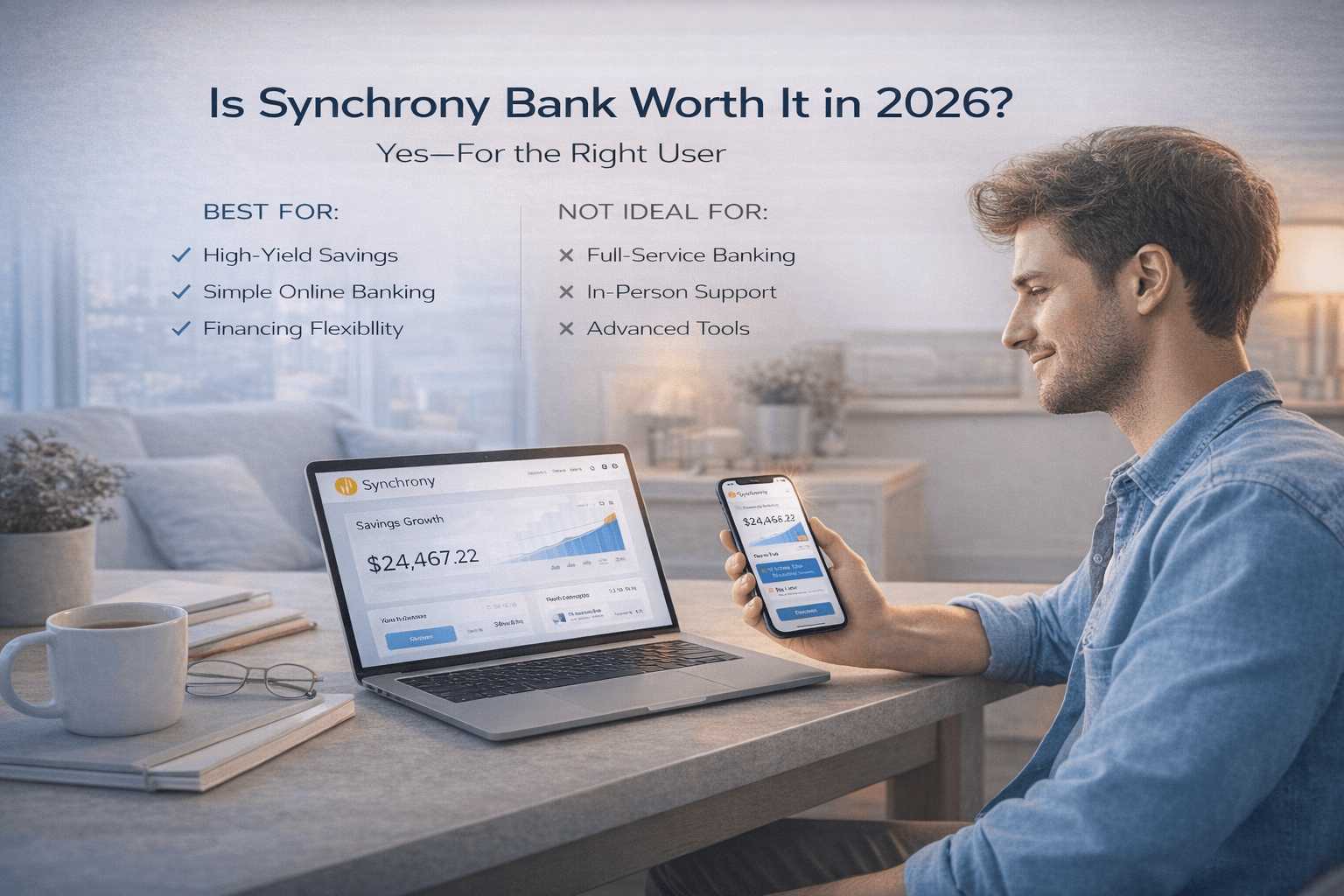

Final Verdict: Is Synchrony Bank Worth It in 2026?

Short answer: Yes — for the right user.

Worth it if you:

- Want top-tier savings rates with no fees

- Don’t need a checking account

- Prefer simple, online banking

Not worth it if you:

- Need a full-service bank

- Prefer in-person support

- Want advanced financial tools

Bottom line:

Synchrony Bank is one of the best high-yield savings-focused online banks in 2026. It’s not a complete banking solution — but as a place to grow your money or finance purchases, it’s extremely competitive.