Most people don’t go to Credit Karma because they’re passionate about credit scores.

Usually something else triggers it.

Maybe you’re buying a car.

Maybe you’re thinking about applying for a rewards credit card.

Maybe a mortgage broker casually mentions your credit score and suddenly you’re wondering if you’re about to get approved or rejected.

That was exactly our starting point.

We weren’t looking for another financial app.

We just wanted to see our credit score.

What happened next is probably why Credit Karma has become one of the most popular financial platforms in America.

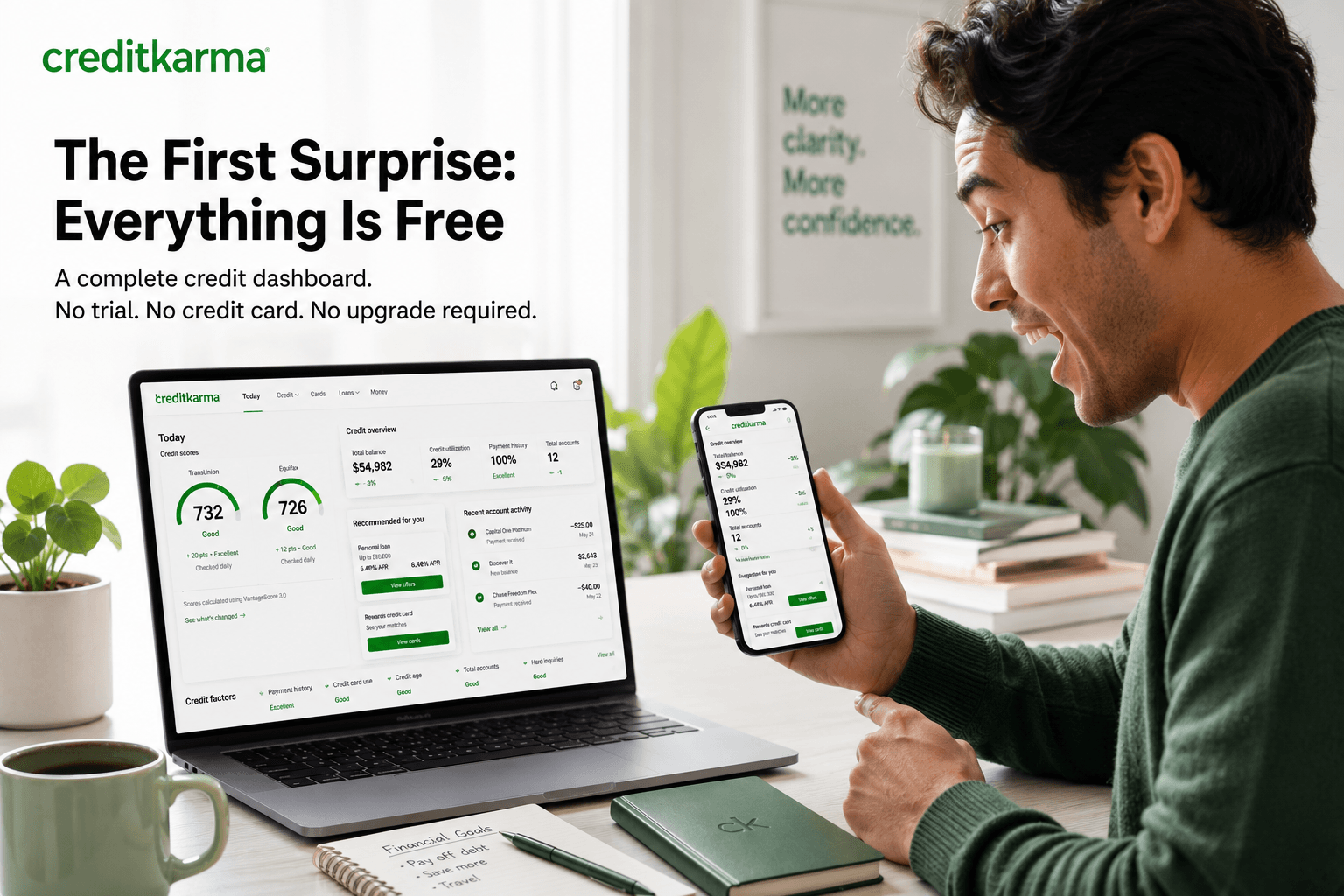

The First Surprise: Everything Is Free

The sign-up process feels almost suspiciously simple.

No trial.

No credit card.

No “upgrade to premium” popup waiting around the corner.

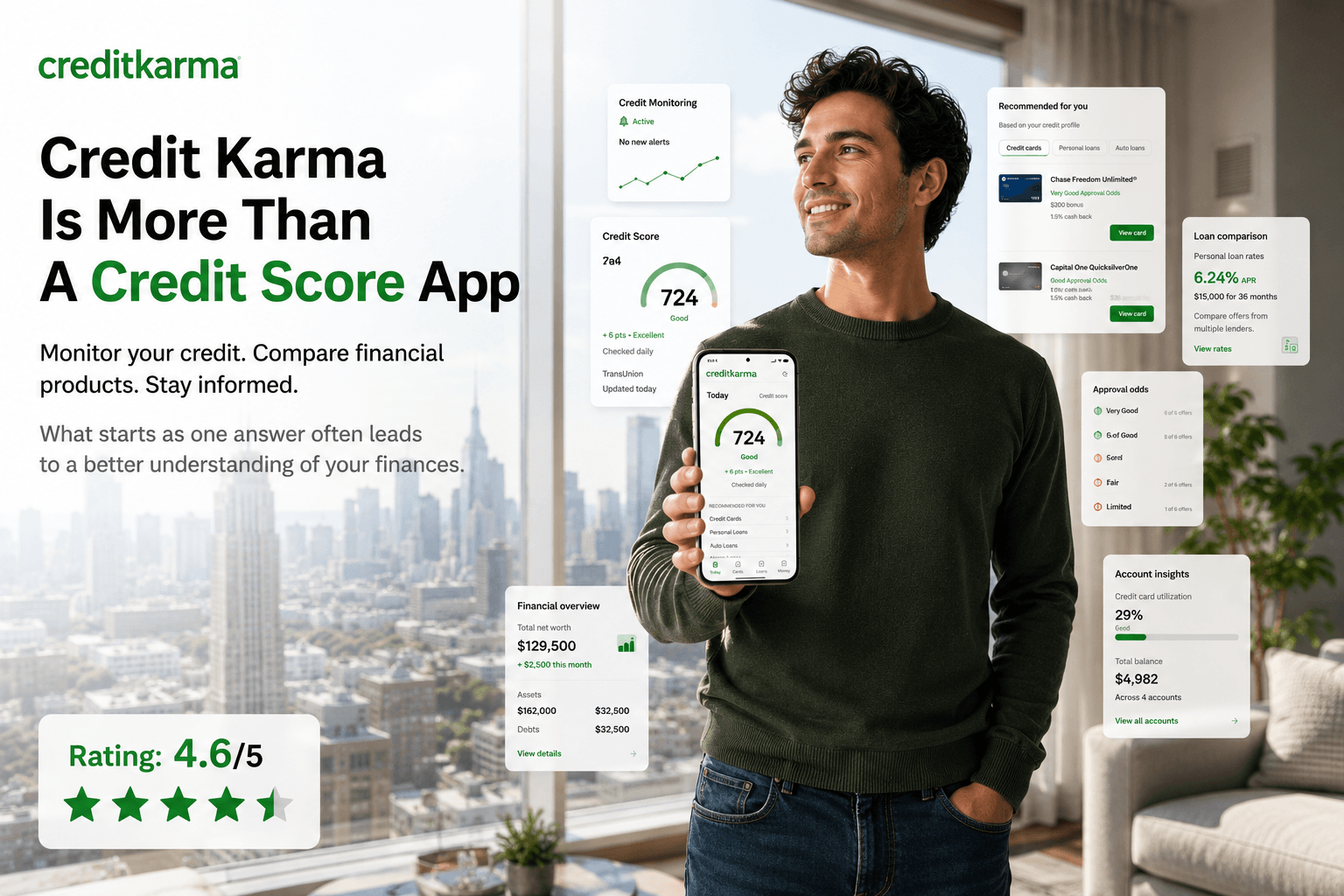

Within a few minutes we were looking at a full credit dashboard.

Not just a score.

A complete picture.

Accounts.

Balances.

Credit utilization.

Payment history.

Recent changes.

Potential problem areas.

For something that costs absolutely nothing, the amount of information is surprisingly substantial.

And that’s when the rabbit hole starts.

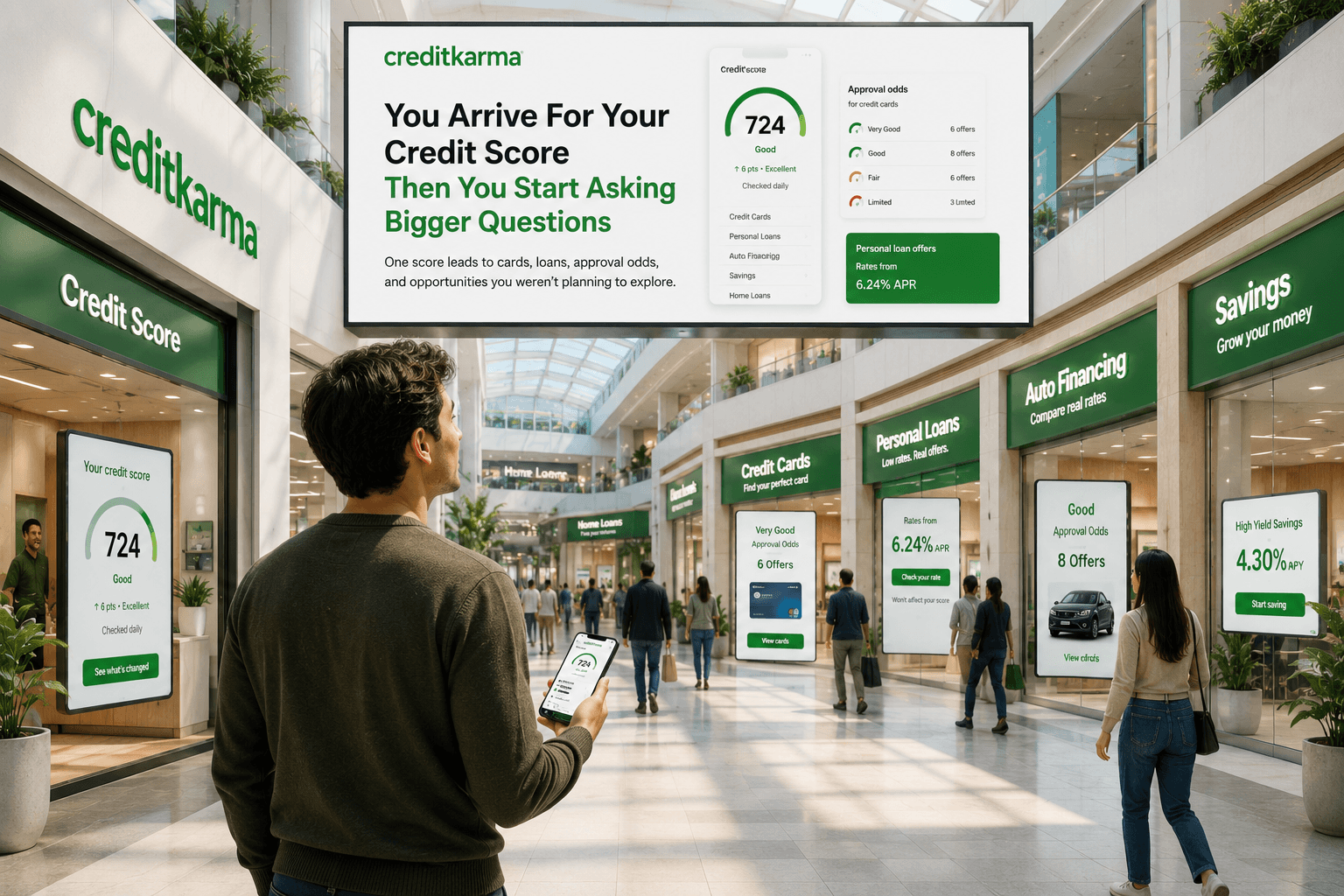

You Arrive For Your Credit Score

Then You Start Asking Bigger Questions

The moment you see your score, a new thought usually appears.

“Okay… is that good?”

Then:

“Could it be better?”

Then:

“What happens if I apply for a new credit card?”

Before long you’re clicking through recommendations, comparing approval odds, and exploring offers you probably weren’t planning to look at ten minutes earlier.

This is where Credit Karma becomes less of a credit-checking tool and more of a financial shopping platform.

The experience feels a little like walking through a mall.

You enter through one door but end up browsing several stores.

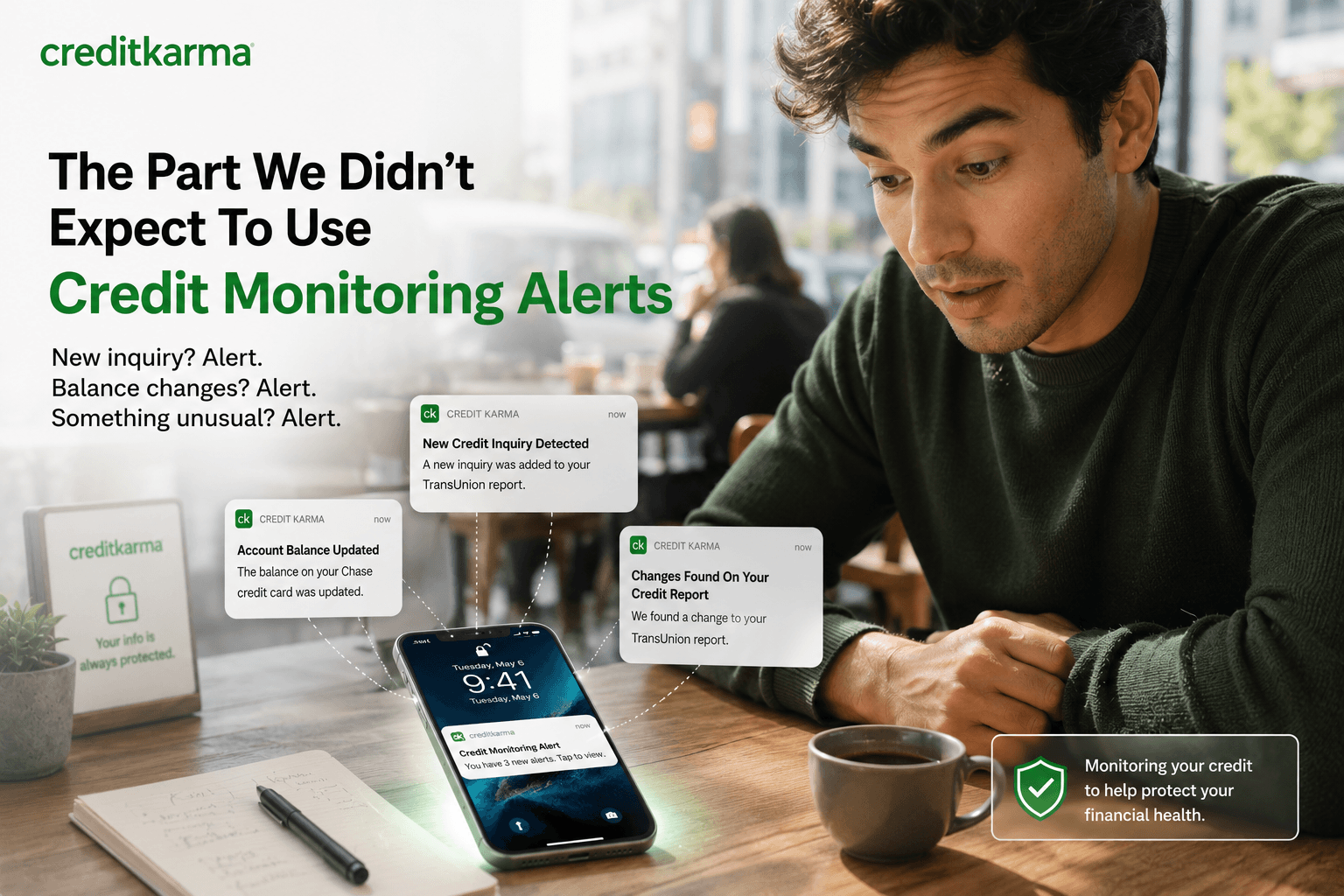

The Part We Didn’t Expect To Use

The credit monitoring alerts.

Most people ignore these when they first sign up.

We did too.

Until we realized how useful they can be.

New inquiry?

Alert.

Account balance changes?

Alert.

Something unusual appears on your report?

Alert.

It’s one of those features that doesn’t feel important until the day you actually need it.

Then it suddenly becomes the reason you keep the app installed.

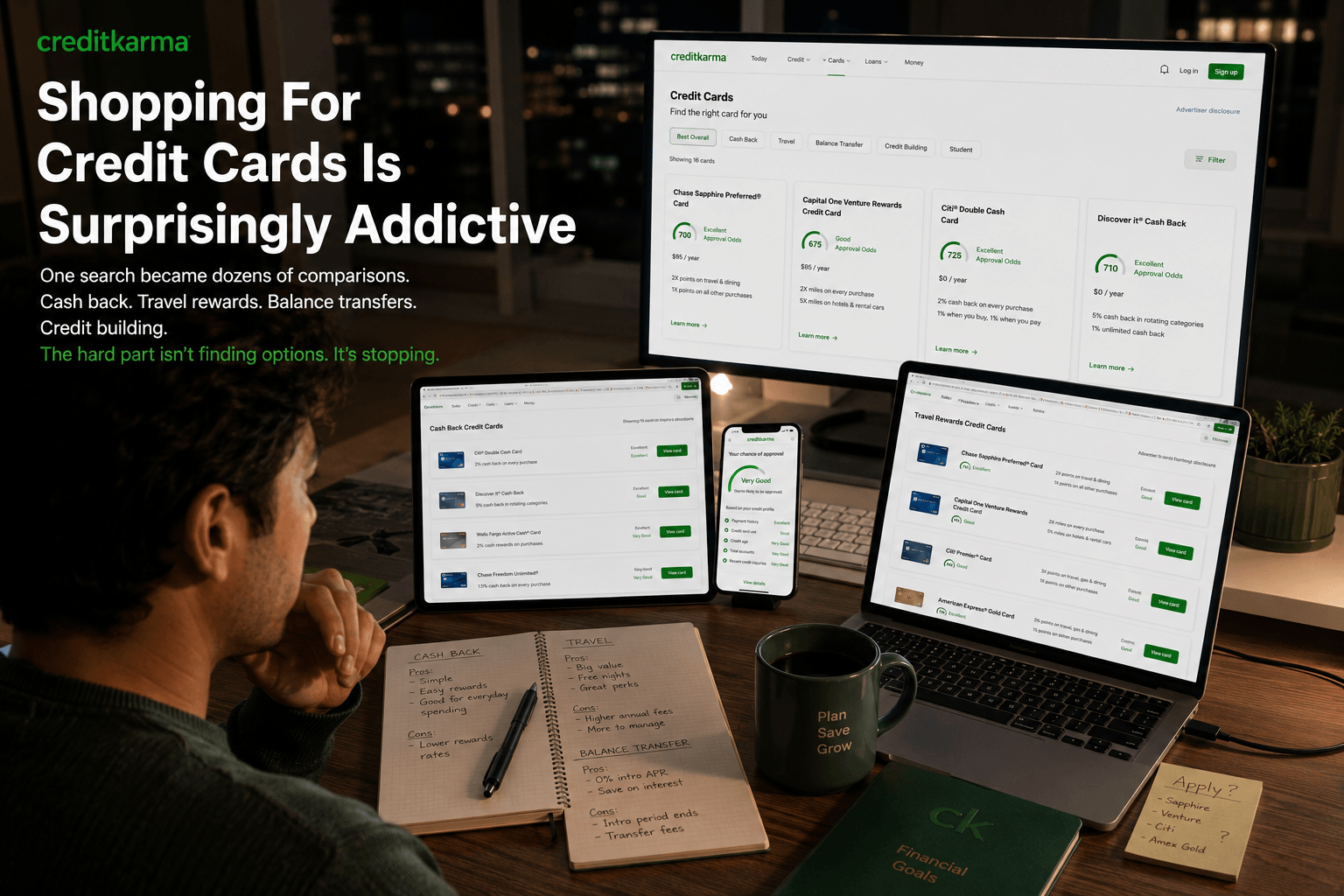

Shopping For Credit Cards Is Surprisingly Addictive

One thing Credit Karma does exceptionally well is turn a normally boring process into something approachable.

Instead of spending hours bouncing between bank websites, you can browse dozens of cards in one place.

Cash back cards.

Travel cards.

Balance transfer cards.

Student cards.

Cards for rebuilding credit.

You start with curiosity.

You leave with twenty browser tabs open and a much better understanding of what’s actually available to you.

Whether that’s productive or dangerous depends entirely on your self-control.

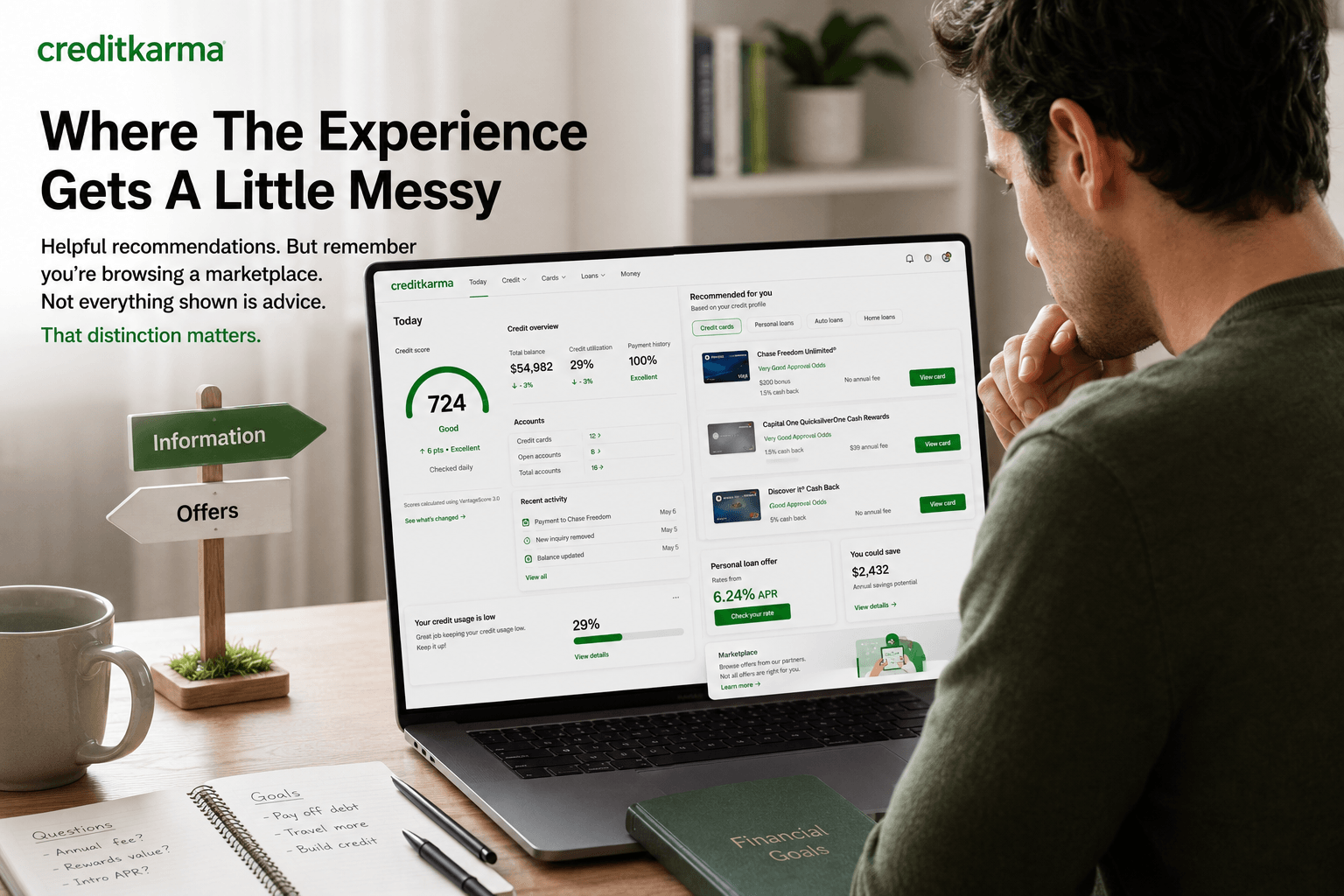

Where The Experience Gets A Little Messy

Not everything is perfect.

At times the platform can feel like it’s trying a little too hard to show you new financial products.

That’s understandable.

It’s how Credit Karma makes money.

The recommendations aren’t necessarily bad.

In fact, many are relevant.

But it’s worth remembering that you’re browsing a marketplace, not getting advice from a financial planner.

That distinction matters.

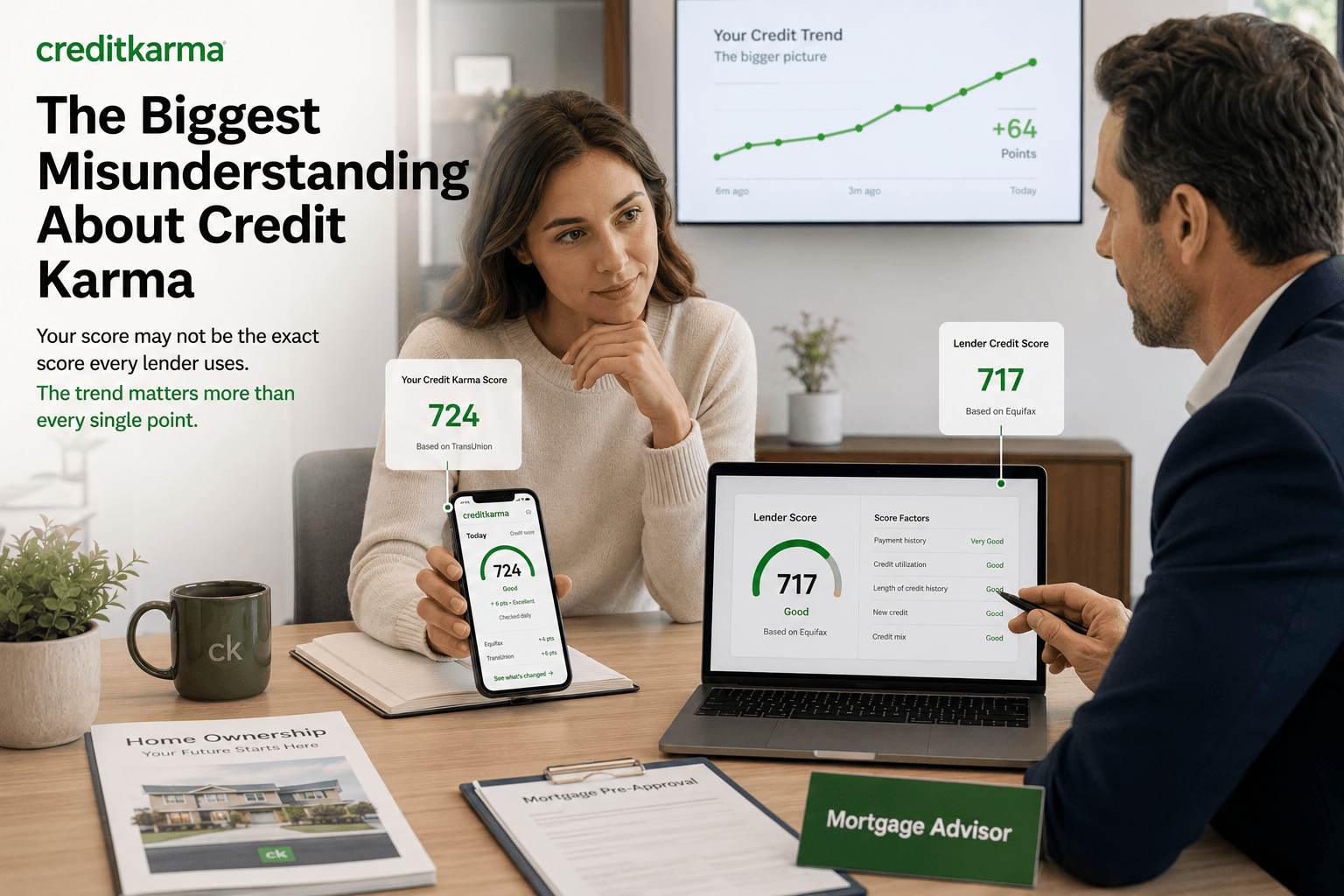

The Biggest Misunderstanding About Credit Karma

Many people sign up expecting the exact score a lender will use.

That’s not always what happens.

Your Credit Karma score can be slightly different from the score used by a mortgage lender or credit card issuer.

For most people this isn’t a huge problem.

The trends matter more than the exact number.

Still, it’s something worth knowing before you obsess over every single point.

Would We Actually Keep Using It?

Honestly, yes.

Not because it’s the most advanced financial tool available.

And not because it provides every possible credit score.

We’d keep using it because it solves a simple problem exceptionally well.

It makes understanding your credit feel easy.

Most financial products make people feel confused.

Credit Karma generally does the opposite.

You can check in for thirty seconds, understand what’s happening, and move on with your day.

That’s a surprisingly valuable experience.

Final Verdict

Credit Karma is at its best when you stop thinking of it as a credit score app.

It’s really a financial discovery platform.

You arrive wanting one piece of information.

You leave understanding a lot more about your financial situation than you expected.

For people who want a free, easy way to monitor credit, compare financial products, and stay informed, it’s difficult to find a better option.

Would we use it ourselves?

Absolutely.

Would we pay for it?

Thankfully, you don’t have to.

Rating: 4.6/5

★★★★½